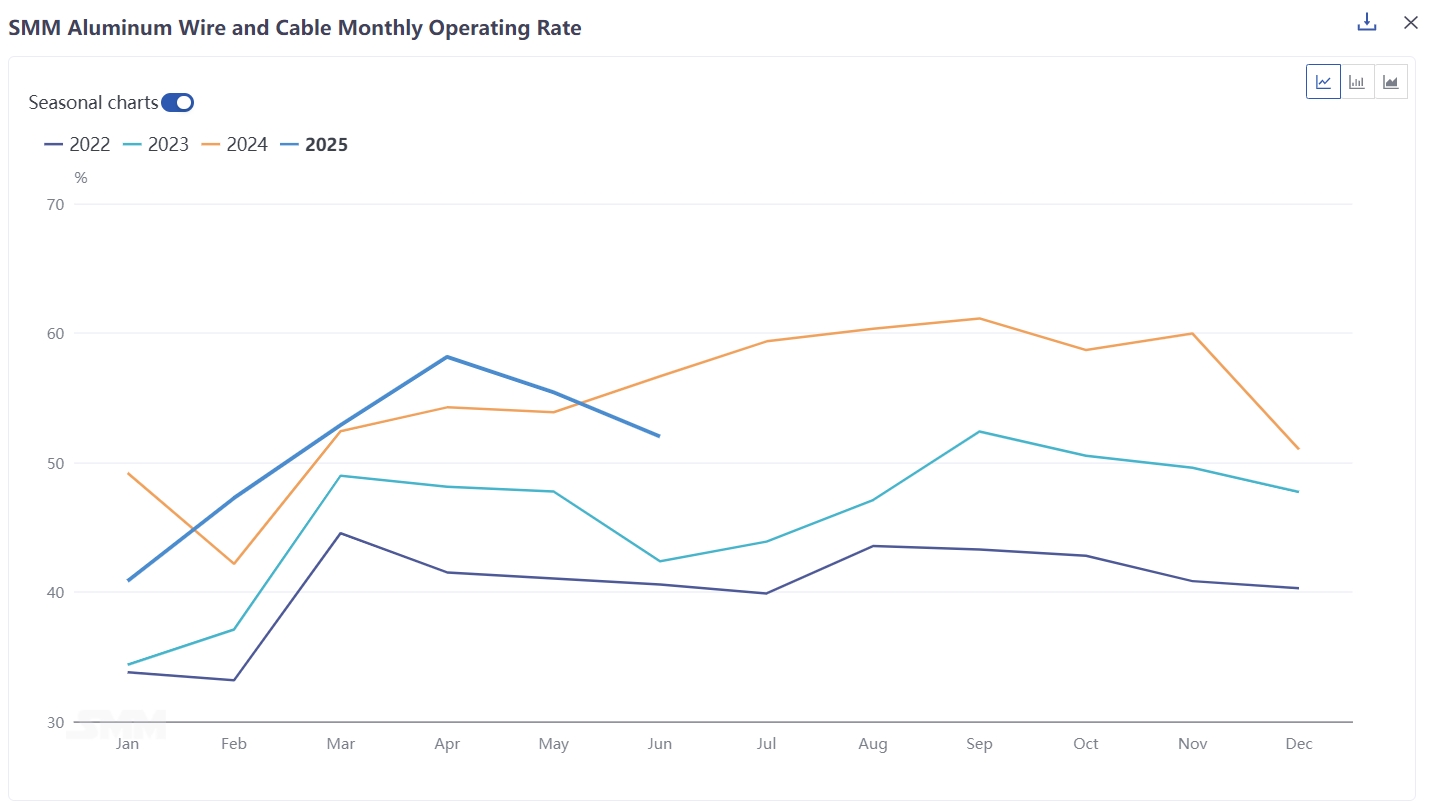

According to SMM statistics, the composite operating rate of the domestic aluminum wire and cable industry in June 2025 was 52.01%, down 3.4% MoM from May and 4.65% YoY from June last year. From the perspective of enterprise scale, the operating rate of large enterprises decreased by 2.4% MoM to 68.53%, that of medium-sized enterprises fell by 3.2 MoM to 45.76%, and that of small enterprises decreased by 10.2% MoM to 16.95%.

On the enterprise side, the days of raw material inventories were recorded at 3.77 days, down 3.19 days MoM, and the days of finished product inventories were recorded at 4.83 days, down 0.52 days MoM. Looking back at June, due to the aluminum price fluctuating at highs and the slowdown in the pace of terminal cargo pick-up, both raw material and finished product inventories fell. Looking ahead to July, considering the current slowdown in the matching speed of orders from State Grid, the lack of a clear recovery rhythm in end-use demand, and the continuous high aluminum price suppressing enterprises' willingness to produce, it is expected that the raw material and finished product inventories of enterprises will continue to decline in July.

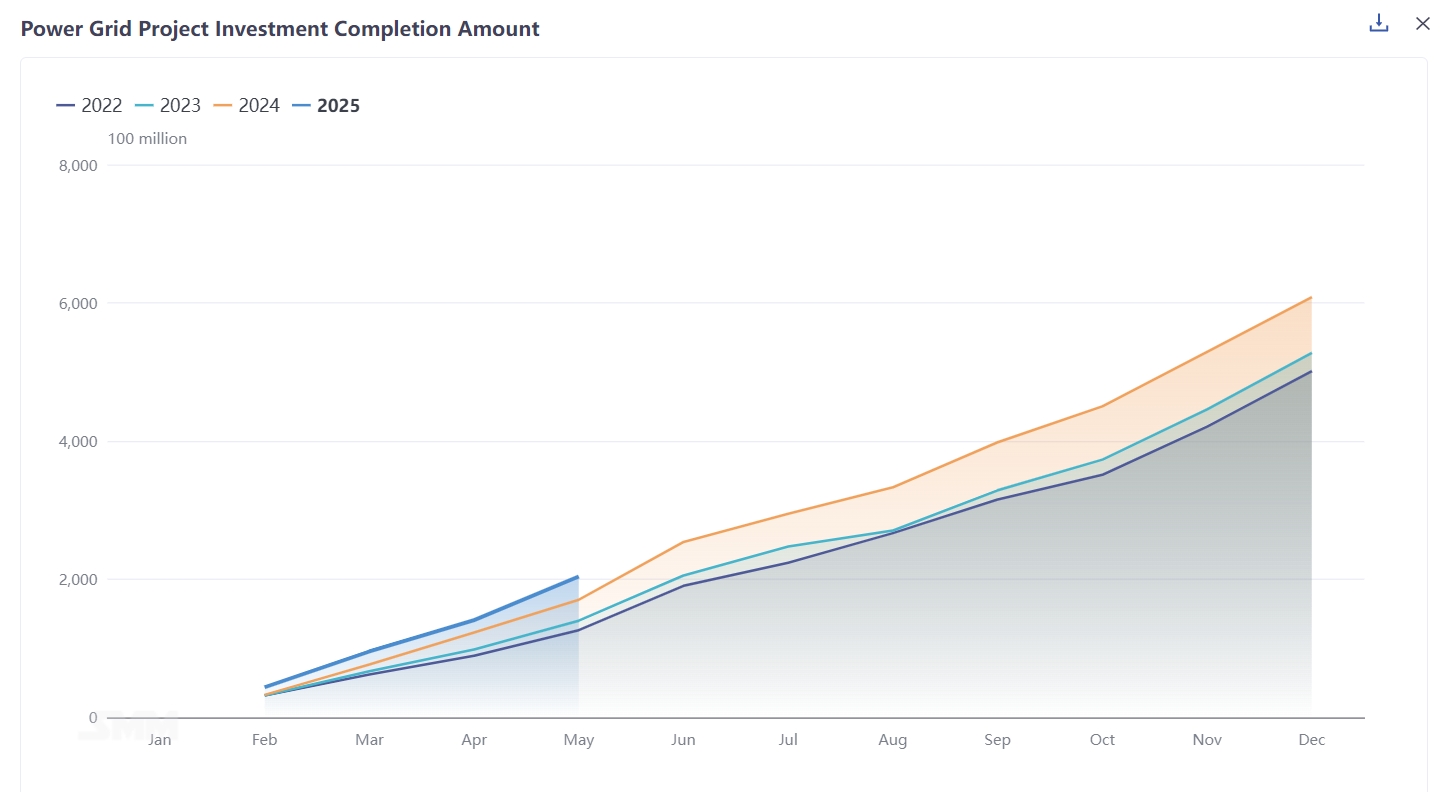

At the order level, in terms of power grid investment, the completed investment in power grid projects in May was 47.4 billion yuan, up 14% YoY, and the completed investment in power grid projects from January to May was 170.3 billion yuan, up 21.6% YoY. Power grid investment is progressing in an orderly manner and is expected to complete the targets set at the beginning of the year ahead of schedule. However, it is worth noting that the tendering rhythm of State Grid lines slowed down in June, and enterprises also need time to digest the orders won since H1. Therefore, it is expected that the speed of new orders from State Grid will continue to slow down in the short term. Due to the recent approval of two new UHV lines in the industry, it is expected that State Grid will continue to issue orders for relevant line materials after August, and State Grid orders will still be considerable in the medium and long term. In terms of PV installations, the new PV installations in May were 92.92 GW, a surge of 388% YoY, and the new PV installations from January to May were 197.85 GW, up 150% YoY. In terms of wind power installations, the new wind power installations in May were 26.32 GW, up 801% YoY, and the new domestic wind power installations from January to May were 46.28 GW, up 134% YoY. Due to the approaching of the "531" policy period for PV, there has been an explosive increase in new PV installations in the short term. However, in the long term, the short-term increase may pre-empt market consumption, and orders for PV and wind power-related cables may weaken in H2, with order performance possibly falling short of H1. In terms of exports, customs data shows that China's aluminum wire and cable exports reached 28,800 mt in May 2025, up 35.2% MoM and 71.4% YoY. From January to May, cumulative exports totaled 111,600 mt, a 26.5% increase compared to 88,200 mt in the same period of 2024. From the perspective of product structure, steel-core aluminum stranded wire exports reached 16,400 mt, up 5.8% MoM, while aluminum stranded wire exports reached 11,200 mt, up 112% MoM, accounting for only 27.3% of the total. From the product structure perspective, overseas power grid construction demand remains stable, with the increase mainly involving aluminum stranded wire. Meanwhile, due to war-related factors, Pakistan's export volume has significantly increased, driving domestic aluminum wire exports. Considering the macro situation and overseas demand, it is expected that aluminum wire and cable exports will be higher than the same period in previous years.

SMM believes that the operating rate of the aluminum wire and cable industry still has a weakening trend in the short term. However, due to the backlog orders held by enterprises, the downside room for operating rates is relatively limited. Despite the industry's shift into a cycle of slower terminal cargo pick-up, leading enterprises can still maintain stable operations due to rigid demand, while small and medium-sized enterprises still lack the willingness to operate due to thin profits, dragging down the industry's operating rate trend. SMM predicts that considering the progress of power grid projects this year, orders for ultra-high voltage and power transmission and transformation projects are expected to enter an accelerated cargo pick-up stage in August. The operating rate of the industry will still have bottom support in the second half of the year. Therefore, it is expected that the industry's operating rate will remain weak in the short term, still waiting for the arrival of the next cycle.

![Aluminum Scrap Prices Follow Upward Trend but with Regional Divergence Market Supply Increases [SMM Cast Aluminum Alloy Morning Comment]](https://imgqn.smm.cn/usercenter/wStpx20251217171650.jpg)